Blockchain

according to Stable Diffusion 2.1

Blockchain has emerged outside of the traditional capitalist logic, but is now one of the most hyped technologies upon which new and old enterprises promise to realize disrupting ways to achieve future. Nonetheless, just like other jargons emerging from the buzzing innovation-centered discussions of international capitalism, real applications of technical know-how may be more limited than marketed. However, unlike other chattered applications – such as artificial intelligence, big data, machine learning, data mining, 5G – blockchains have the potential to be a fully operational part of every organization, coordinating and timing labor and exchanges with its underlying institutional identity. These motivations spark interest around blockchain as a new institutional technology (Davidson, De Filippi and Potts 2016), making it even more relevant to understand when organizations are eligible to introduce such a mechanism.

Among a wide range of theories, transaction economics theory allows for a more thorough analysis of organizations. Economic sociology literature has scattered the focus of analysis, for one thing, on the underlying institutional culture – contemplating different approaches within (Podolny 1993, Polanyi 1945, Fligstein and Mara-Drita 1996) – or on socio-technical agency (Callon 1998, Preda 2006). On the other hand, sticking to the path traced by economics, TCE shares the same vision of goal-oriented, optimizing actors, albeit adopting a behavioral approach when addressing contractual relations, reviving the interpretation firstly endorsed by Herbert Simon. Built upon exchanges, organizations that take advantage of new technologies as well as of traditional ways of dividing labor struggle with the limits that are imposed by human nature. In fact, Williamson interprets the basis of the economic organization as a conjunction of both human and transactional factors (Williamson 1973). On the one hand, bounded rationality can pose a great limit to the human ability to receive, store, retrieve and process information without errors, with the chance of effecting interfirm exchange and the competitive equilibrium altogether. On the other hand, opportunism – as it will later described – narrows the spectrum of choices when acting in an uncertain environment. Furthermore, from Williamson’s perspective, technological reliance in organizations can exist albeit less relevant than the other factors previously described. Recent studies and emerging corporate realities challenge this assumption, bringing technology in the spotlight as a peculiar way of organizing transactions.

The first section will review the transaction cost economics theory, with a particular focus on the contractual schema described by Williamson based on the early studies of I.R. Macneil. The emerging model focuses on the institutional arrangements between actors (Williamson 1993), without posing too much attention on the institutional environment therein. Although organizational atmosphere may indeed play an important role in influencing the preferences of actors – for example making profit yield to other types of satisfaction –, other decisional moments are more appropriate for studying blockchain. In the second section, we will further develop the insightful intuitions brought by a vast array of scholars, including Primavera De Filippi, focusing on the relevance of trust opposed to confidence for the settling of institutional arrangements. From this, it will be possible to contextualize trust and confidence as the underpinning of social exchange when technology is considered. A practical and straightforward identification of the pertinent elements of the blockchain will be performed. The conclusions will follow in the last section, with a summary of the previously exposed arguments, highlighting the importance of analyzing the underlying existing organizational realities.

“Recent studies and emerging corporate realities challenge this assumption, bringing technology in the spotlight as a peculiar way of organizing transactions.”

Fad or a real opportunity?

TCE, contracting and coordination

Williamson described a model of possible interpretation of contracting mechanisms taking place between actors, with the goal to underline the difference governance structure emerging from such arrangements.

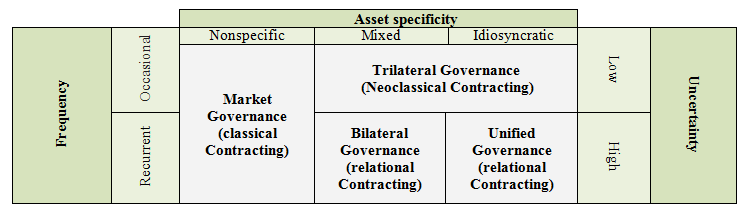

Transaction costs economics (TCE) considers a diverse array of elements in the making of transactions, with particular regard to asset specificity – that juxtaposes idiosyncratic1 goods to standardized ones –, uncertainty – that incites or hinders opportunism – and frequency – that promotes a tighter dependence between actors (Williamson 1979). Uncertainty – related to the frequency with which transactions repeat and the degree to which investments are idiosyncratic – contributes to defining the essence of a transaction and shape the associated governance structure.

Another concept fills in the blanks: opportunism is a central concept when analyzing economic activities that regard transaction-specific investments in human and physical capital. Opportunism is defined by the author as an extension of the simple self-interest seeking rationale, in order to also include trickery and slyness from at least one of the sides involved (Williamson 1979). This can bring actors to reject those values associated with integrity in order to realize individual gains. The strategic disclosure of asymmetrically distributed information is further facilitated by the initial contract (Williamson 1973), even in cases of relational contracting.

Still, the goal of actors described by TCE is the optimization of costs (also intended as the enhancement of the Total Factors of Production – TFP), thought as composed of two distinct elements: production costs and transaction costs. The former relate to those core actions that are necessary for running the economic activity. The latter are defined as those costs concerning the organization of the economic activity, whether they are before the transaction or after the transaction. The different arrangement of transaction costs makes the emergence of a specific governance structure over others more likely. The institutional matrix within which transactions are negotiated and executed varies therefore with the nature of the transaction itself. As Williamson puts it, “transactions, which differ in their attributes, are aligned with governance structures, which differ in their adaptive strengths and weaknesses, so as to accomplish a transaction cost economizing result” (Williamson 2008, p. 8). For example, cost economies in production will obtain for highly specific activities only if the supplier invests in a special-purpose plant and equipment or if his labor force develops particular skills in the course of contract execution, binding therefore his interests to those from the buyer’s side. The anticipation of a tight long-term relationship between buyer and supplier is needed to encourage idiosyncratic investments.

Some authors criticize the assumption that actors seek the cost economizing result, blaming TCE to fall into a fallacious functionalist approach that views market rules and roles as reflections of the efficiency demands of the market (Abolafia 1998). Against TCE and other agency theories, Callon and others suggest that social arrangements should be seen as reflecting power, status and historical contingencies in the market, creating episodes of path dependency. Nonetheless, despite this stream of thought correctly considers the market as socially constructed over time, it is unquestionable that actors may still find themselves in that specific arena with specific rules to which they must behave accordingly.

Moving on, Williamson repeats the delimitation between the discrete-transaction and the relational paradigms operated by the Scottish American legal scholar I.R. Macneil (Williamson 1979). The former is widely adopted as an interpretive framework both in law and economics and endorses clear agreements on the one hand and clear performance and outcomes on the other hand. The latter finds its underpinnings in the idea of highly specific relations between actors organized in hierarchies. As the author suggests, the study of discrete contracting should be secondary in relation to the focus on the contractual purposes. Inasmuch as different transactions have intrinsic characteristics also related to the nature of the assets exchanged, each stipulated contract is subject to and reflects the relationship rolling out between the actors.

The unassisted market and classical contracting

Letting k be the measure of asset specificity, we can reason about it as the starting point of the model, with its relevance triggering the further entry of other elements to ponder. Asset specificity determines the range of activities across which an asset can be suited in order to perform more than just one duty. More specifically, assuming an asset to be provided by a highly flexible, extensively used, general-purpose technology for which k=0, the low specificity of the asset pushes the model towards what Williamson describes as the “unassisted market” (Williamson 1979, Williamson 2008). Items that are unspecialized among users pose few hazards, since buyers in these circumstances can easily turn to alternative sources and suppliers can sell output intended for one buyer to other buyers without difficulty (Williamson 1981). The kind of technologies we intend here are those with the ability to be fitted across many sectors of the economy and that creates many spillovers due to their versatile nature. These technologies can be described as performing generic functions that lie at the heart of production systems, making them general in extent and giving them the chance to be easily adapted on a wide scale (Bresnahan and Trajtenberg 1995). The benefit of introducing electricity or computers accrues to all economic activities that use those technologies in a distributed market governance, due to enhanced factors of production capable of putting out an augmented marginal revenue. For example, railways, electricity, the computer, the internet, artificial intelligence, all had broad revolutionary applications. As highlighted by Breshnan and Trajtenberg, transactions of general-purpose technologies do not engage additional specific assets, making the identity of parties less relevant.

For an organization, the incentive to put in place its own produced general-purpose technologies is very low, due to the high availability on the market of the given technology along with a potential complexity of realization. If the relationship between the GPT and its users is limited to arms-length market transactions, there will be “too little, too late” innovation in both the GPT and the application sectors (Bresnahan and Trajtenberg 1995).

As Macneil suggests, this specific type of market governance is based upon the common use of classical contract law. The key feature of such contracts is the enhancement of presentiation, namely the act of depicting something as perceivable, effective and concrete as if it were in the present. From this stems the consideration of the original agreement as the reference point for future developments. The aim of such contracts is to achieve reduced uncertainty and portrait information as complete as possible, in order for bounded rationality not to obtain. In this case, given the higher degree of generality of the asset, frequency does not play an important role in the shaping of the underlying governance.

The economic counterpart of complete presentiation is contracting based on contingent claims, a contractual model adopted in conditions of uncertainty to reduce risk with which actors insure themselves against a negative event. For example, the value of a crop will depend on weather conditions, urging farmers to ponder the possibility to enter into a contingent contract that guarantees them a certain sum in the event of high drought (Airoldi, Brunetti and Coda 2005). Even more precisely, the supply of a good or a service can be discounted and described taking into account several future eventualities, with an impact on price and terms.

In this perspective, markets can manage economic knowledge – and structure relationships – through the price system, making coordination possible. As Hayek argues, the “limited individual fields of vision sufficiently overlap so that through many intermediaries the relevant information is communicated to all”, allowing the market to act as a single entity (Hayek 1945). Again, attenuated uncertainty translates in the identity of the parties being irrelevant, making this model correspond with the ideal market transaction in economics.

Furthermore, written formal agreements cast their shadow upon verbal informal terms when it comes to individuating rights and obligations in case of controversy. Finally, in the case of unexpected events, remedies to negative impacts have been already set, making the allowable margin of freedom or variation from the initial agreement way less extended. Although incentives regarding requisites might be provided if long-term contracts were negotiated, such contracts would be necessarily incomplete when dealing with idiosyncratic relationships because of human bounded rationality.

Safeguards, trilateral governance, and neoclassical contracting

On the other hand, assets that must be provided with a special purpose technology for which k>0 leads to more idiosyncratic transactions. This model incentivizes a higher degree of continuity compared to the previously described one, since the higher specialization in a restricted market makes the availability of traders on both the supply and the demand side lower. In this specific context, bilateral dependencies emerge sided by the need to look after specific investments. In this case, presentiation becomes harder – if not impossible – for long-term contracts and the proper remedies needed in case of unfortunate events cannot be known beforehand. In case of higher uncertainty, disputes related to the terms may rise. Now, if we assume s to be the extent of “safeguards” aimed to reduce those disputes (i.e. penalties, verification procedures, incentives to behave morally, specialized resolutions, but also cryptographic validation), we can trace more additional situations: one in which s=0 and one in which s>0. The importance of those safeguards is more than just psychological, hence affecting the genuineness of the involved transactions.

When s=0, uncertainty becomes stronger and the reliance of one actor on the other one is not backed up by insurance mechanisms, leading to “unrelieved hazards”. This can have effects on the price charged by each one of the two parties, making it drift away from market price in order to have a higher monetary compensation for those hazards that loom upon the horizon. Moreover, the case in which transactions are forgone altogether is also a possibility. In this specific case, it is likely that the adopted contractual model will still be the classical contract law, but with an increased price to reflect the added risk coming from the unstable governance. Litigation is contemplated as a possible solution to emerging disputes, albeit as a last resort. Litigation is wielded with the only purpose of negotiating claims and further efforts to preserve the relation are not made because the relation is not independently valued (Williamson 1979). Set in front of a public court, we can evidently assume that relationships are effectively shattered if a dispute reaches litigation.

This instability and the increased reliance of the two parties onto each other are the reasons that pushes actors towards the introduction of safeguards, with s>0. From this point onward, even if each possible outcome and behavior cannot be forecasted, trust supplants power as the key concept underlying relations, albeit in different degrees of relevance. In comparison to the market model based on classical contracting, trust plays a stronger role due to the interdependence between actors when increasingly more idiosyncratic assets are onstage.

The safeguards embraced here take the form of inter-firm contractual safeguards as well as the introduction of arbitration. In fact, arbitration relies on third-party assistance for resolving disputes and runs as an alternative candidate to litigation. Here, presentiation is still difficult, but a third party may be now entailed, leading to the neoclassical contracting model described by Macneil. Nonetheless, trilateral governance only comes in useful when occasional transactions of a moderate to high degree of idiosyncrasy occur. Due to the occasional nature of exchanges, uncertainty is smaller than if recurrent exchanges between the same two parties were needed.

Relational contracting

On the other hand, when the asset specificity increases as well as the recurrence of the exchanges, additional uncertainty impends. The non-standard nature of transactions emerging, for example, from recurrent exchanges of customized material or from the necessity of supporting intermediate production market transactions is one of a more specific nature. We now approach the relational contracting models, reflecting the “increased duration and complexity deriving from a […] mini-society with a vast array of norms beyond those centered on the exchange and its immediate processes” (Williamson 1979). The reference point is shifted towards the relation as it has developed, which it may or may not include the original agreement.

In case of mixed transactions, which imply a lower specialization of human and physical resources, economies of scale may be achieved through outside procurement. Transactions of the recurrent kind where mutual interests are laid and that are overhanged by changes in the external environment can realize themselves into bilateral governance. The main contract tool in this context is represented by escalation clauses, to wit, terms that guarantee a change in the agreement price once a particular factor beyond control of either party affecting the value has been determined (i.e. inflation). For example, if a company B uses a resource provided by A to produce a component and the contract between the two parties allows for a partial relief of the price of the resource in case of exogenous impact on sales of the component, then we can describe that as a bilateral governance. Flexibility and trust are here the key concepts. Nonetheless, despite committed bilateral efforts to craft this kind of safeguards, unbearable high-priced failures may occur, leading to the transaction to be taken out of the market and organized beneath unified ownership instead.

If instead on market support, an organization were to rely on administrative structures, it would in every respect actualize a hierarchical structure. Hierarchies have advantages related to the more direct and straightforward supervision of individuals (Alchian and Demsetz 1972), with achieved transactional optimizations when k>>0 occurs in presence of highly idiosyncratic transactions. Firms arise when tasks are a technological whole and conjoint efforts making individual contribution as a whole. For example, by working together, two individuals can load a cargo onto a truck in shorter time than if they labored separately. The product of their efforts exceeds the sum of their individual contributions, making it harder to tell who the free rider is. As previously showed, opportunism is tightly related to the nature of the investments and it is generally very costly to distinguish opportunistic from non-opportunistic behaviors. Opportunism is thus encompassed and overcome taking advantage of incomplete contracts (Sinclair, De Filippi and Potts 2018). The transaction costs of opportunism are internalized and put under control mechanisms inside the firm, such as ways of discriminating wage in supervisor-subordinate relations (Williamson 1973).

To conclude, this model relies on the assumption of bounded rationality of actors, reminding us that also other human factors play a crucial role, such as opportunism and “atmosphere” – or institutional environment. Indeed, opportunism and trust are tightly interwoven, but this all boils down to the possibility to operate guileful behaviors in order to take advantage of misplaced trust. From this point of view, organizational forms are shaped by the need to control opportunism, ultimately caused by the emergence of idiosyncratic investments that locks in the economic actors, as well as by the the intent of exploiting trust and asymmetrical information. Bounded rationality and incomplete contracts make trust and integrity one of the few ways to overcome opportunism in the TCE perspective.

The blockchain technology hinders the possibility for opportunism, enhancing what De Filippi et al. describe as the confidence in the computational model (De Filippi, Mannan and Reijers 2020). Blockchains are an additional way for controlling opportunism, eliminating the need for trust with using the not-anymore incomplete smart contracts.

Nonetheless, the cultural context in which transactions are embedded can make the trust placed on actors still relevant. From this perspective, trust and confidence are two distinct concepts that find their respective roots in a long historical debate.

In the next section we will take a look at how blockchain relates to trust and how it possibly paves the way for new modes of governance.

“[…] organizational forms are shaped by the need to control opportunism, ultimately caused by the emergence of idiosyncratic investments that locks in the economic actors, as well as by the the intent of exploiting trust and asymmetrical information.“

Trust and contractual basis for governance in the blockchain

Several elements should be taken into account when analyzing the relevance that blockchains can have for organizations. Firstly, reliance on the system can be expressed by a dilemma regarding the true connotation of trust, juxtaposed to a sharper definition of confidence. The two concepts are different and carry distinct implications when such a technology is invoked. Secondly, set of rules crystallized into contracts can be one among the main drivers of organizations. How contracts interact with the concept of trust – and confidence – is vital for analyzing the possible governance arrangement thereof. This leads to asking if confidence in the blockchain system due to complete information is enough to completely overcome opportunism. Thirdly, governance and consensus mechanisms are tightly interwoven and shape the characteristics of blockchains. Permissionless and permissioned blockchains are the two most debated forms of blockchains, but it is still relevant to take other organizational elements into account.

Trust vs Confidence

On the one hand, trust can be regarded as a relationship between two or more parties, whereby one party (the trustor) decides to rely on another party in uncertain conditions (the trustee), putting himself in a vulnerable position in order to achieve a particular task. Hence, trust presupposes awareness of risk, but with the purpose of economizing on resources and reducing the level of involvement. As Williamson and Gambetta agree on the idea on trust, the risk involved in situations of trust derives from uncertainty regarding the future actions of others (Williamson 1993), making the relevance of the institutional framework more important when shaping the arrangement of economic units. In this sense, trustworthiness is differently assessed based on whether the trustee is an individual or an institution. The individual can be thought of as reliable if his reputation is publicly backing him or if evidence of trustworthiness emerge from repeated interaction. But when it comes to institutions, more individuals as well as a cultural background must be taken into account, making things more complex. Nonetheless, the persons involved in the design, production and administration of that system should be still considered as honest and sincere in order to avoid mistrust. Although institutions are made of individuals and one can infer their trustworthiness by interacting with representatives or delegates, in this context, in order to trust an institution, one does not need to understand all the internal working mechanisms of the institution itself, since the governance network in which an institution lays gives additional information. However, I suggest that with open-source institutions which proclaim transparency this may turn out to be different, bringing inside several parties with different interests and possibly exposing the internal equilibrium to popularized lobbying practices that resemble open market competition. To summarize, trust is a decision taken towards another actor in a context of uncertainty that originates from the integrity of interpersonal relations and creates subsequent asymmetry (De Filippi, Mannan and Reijers 2020).

On the other hand, confidence does not need the complete recognition of agency and simply arises from the cognitive process of one single agent (ibidem). This is made certain by the fact that the condition of risk is here absent and that has given way to a sense of predictability of regulated processes. Confidence can be either directed or undirected and information asymmetry is here missing. In this sense, there is no need to put trust in a system that is completely transparent and whose mechanisms are well known and publicly understood. Since all the nodes in a blockchain network can personally verify that all the information held on the blockchain itself is legitimate, anyone can have a high level of confidence that the system will operate as planned. The transparency of the mathematical processes ruling the blockchain system and the monitorability of the hashing algorithms reduce the need for trust, replacing it with a diffused confidence in the system and reducing the risk of individual opportunism.

Nonetheless, trust in developers, maintainers and regulators is needed. A broader definition of confidence would hence mean to ultimately trust the whole assemblage of actors associated with that network. For example, some projects can be by origin a joint effort of a different array of cross-industry actors, just like the Hyperledger project hosted by the Linux Foundation. The open-source project is backed by finance, banking, IoT, supply chain, manufacturing and technology leaders and different interests are hence represented.

Limitations

The contractual application of such confidence principles are smart contracts, complete contracts based on fixed conditions that are coded inside decentralized and shared applications running on the blockchain. These systems are unmediated and operate as a private regulatory framework that has been described as lex cryptographica (De Filippi and Wright 2018, p. 5). By aggregating a range of rules into a set of smart contracts, it is possible to structure a cohesive network of hard-coded relationships that set up the standards and processes that everyone interacting with or taking part to an organization should follow (De Filippi and Wright 2018, p. 133). By the use of autonomous code based on the blockchain, organizations can divide tasks and set up smart contracts that forbid any internal event to happen without the explicit approval of multiple parties. In this sense, the rigidity of a blockchain serves as an additional layer of accountability, creating organizational rules that are unleashed and protected from the internal management within.

As already presented, several theories of the firm aim to resolve the principal-agent problem – raised by the incompleteness of contracts due to bounded rationality – considering trust in the measuring of productive output and when realizing control systems (Alchian and Demsetz 1972, Williamson 1973). Although this would deserve a whole separate dissertation, smart contracts can be intended as complete contracts that significantly reduce uncertainty related to difficult presentiation. In a world of complete information, based on the model of transaction cost economics, every transaction would happen in the market. However, the cost of creating and enforcing contracts has to be taken into account. This creates a situation in which those parts of the organization that can be rendered as complete contracts with low or zero transaction costs are eligible to be brought under a blockchain framework (Sinclair, De Filippi and Potts 2018).

Can blockchain represent a new type of economical organization?

What’s the role of trust in the shaping of relationships over a contractual basis?

Governance and consensus mechanisms

Beyond the dialectics between a general-purpose technology – able to lower production costs following the neoclassical approach – and a technology seen as capable of lower transaction costs, Davidson et al. propose the study of blockchain within the institutional lens, intending the technology itself as a new type of economic institution (Davidson, De Filippi and Potts 2016). Sure enough, we may intend blockchain as a way of organizing labor and economic activity, namely a tool for arranging transactions in order to include transparency and immutability with the aid of a specific technology.

However, the actual introduction of blockchains into organizations has been already discussed, potentially raising some eyebrows also in the technical sector (Dhillon, Metcalf and Hooper 2017, p. 144). It is noteworthy that transaction interdependence and the order in which transactions are performed may impact the eligibility of a system to be blockchain-based. A blockchain is truly fitting when handles a log of transactions with a long history involving multiple users. Also – as the Birch–Brown–Parulava and the Wüst–Gervais models suggest – if the parties on the network have similar motivations, some of the blockchain constructs managing trust can be safely removed. From the very early idea firstly described in the original white paper (Nakamoto 2008), new adaptations of the blockchain technology have evolved, but the underlying components have remained almost unaffected. Different elements can be picked in order to suit the diverse needs and characteristics of organizations.

Architects: The blockchain architect design and builds the software that defines the blockchain network. This may include integrating external data storage, external processors to offload expensive computational processes, and peer relationships with other systems via the blockchain’s system integration functionality. Architects and regulators have the ability to design and settle the underlying principles on which the blockchain will operate when fully functional, shaping the decisional environment of participants.

Operators: Once the blockchain network has been created, operators create wallets to store their credentials that are on-boarded through the management system to create the peer network. This network stores, maintains and updates the blockchain’s distributed ledger.

Users: Users can also join the blockchain by setting up wallets and coordinate to fill their intended roles. This includes developers and regulators, who take a more active role in the blockchain than the regular user.

Developers: In order for the blockchain to have functionalities that the user can use, smart contracts need to be created on the blockchain. Developers design, implement and upload them to the blockchain for end users to interact with.

Consensus: Computational nodes in a system need a mechanism to agree on the current state of the shared information. The idea of consensus is brought in the development of the blockchain in order to allow nodes to control operations performed on the blockchain (Voshmgir 2019). Consensus systems take advantage of the scarcity of computational resources in order to ensure decentralization. The main difference between consensus mechanisms is the way in which they delegate and reward the verification of transactions, making them therefore vital for governance. Proof of work and proof of stake are the two main consensus mechanisms. The former lets the participating nodes – here called miners – race to find an acceptable solution to a complex cryptographic problem whose solution can only be solved by random guessing. When a miner finds an acceptable solution, they create a block and broadcast it to the network. Every other node examine that solution, ensure the quality of the associated information and finalizes the containing block. On the other hand, the latter is based on the number of tokens that a node can put aside in order to create a “stake”. A block forger is pseudo-randomly selected from all of the users who have staked some of their assets, and the selection process is biased based on the size of the stake. For example, Cardano tokens can be also delegated to a specific stake pool in order to increase its probability to be the next validator node. The assets of a proof of stake ledger are therefore dual in nature, acting as both transaction means and participation rights in the consensus protocol.

Different blends of blockchain can be realized by allocating different weight to each actor and component of the network. The very ideas that separate permissionless and permissioned blockchains convey peculiar representations of power among actors, evidently emerged from the proto-liberalist ideology characterizing the subculture of the origins (Jones 2019). Permissioned blockchains often take the form of consortia, historically aimed either to build and operate blockchain-based business platforms to solve a specific business problem (e.g. Digital Trade Chain – focused on cross-border payments) or to develop reusable blockchain platforms based on technical standards (e.g. Hyperledger). Permissionless blockchains do not have only one infrastructure and oftentimes do not have a one shared goal pursued by few individuals.

Similarly to the “software-as-a-service” model, it appears evident how blockchain applications are heavily entangled to the governance of the infrastructure, which can complicate governance models (Rikken, Janssen and Kwe 2019). For example, with different consensus mechanisms, specific governance challenges occur, like “whales” (large token holders) in proof of stake or geographically concentrated mining power in proof of work. Different systems of consensus and different tokens allowing for different rights within the network can be deployed in order to create flexible solutions for the organization in question.

Rikken, Janssen and Kwe further explore the institutional model proposed by Williamson in order to include timelines and decisional steps, pointing at a new model that considers also stages of decision-making as an element to contemplate when shaping the idea of a blockchain application (2019). Yet, there is little to none known practice in blockchain governance and further exploration is needed.

Conclusions

Transaction cost economics provides a good starting point for analyzing opportunism and uncertainty in an organizational system. When studying a blockchain system, uncertainty, institutional environment and specificity of transactions should be taken into account. When challenged with the application of blockchain to our societies, we should consider the characteristics of the underlying organization and the nature of the transactions performed. Secondly, although blockchain has some peculiarities that set it apart from other technologies, trust cannot be completely removed by introducing smart contracts. When talking about a broader adoption of blockchains, already existing governance structures may be brought inside the blockchain system, reflecting already present divides albeit being justified as transparent and equal. This is made possible by the deployment of different systems of consensus and different tokens allowing for different rights within the network.

Too few elements indicate with certainty that blockchain is going to be the ultimate disruptive technology of our century. Yet, in order to best confront the challenges that such a technology poses, a reasoning about the social impact it may have is fundamental. As I may understand it, transaction cost economics should provide an applicable interpretive framework of the organization for gauging exchange reality and knowledge management – hence, to some degree, power.

To conclude, when facing a new blockchain application, it would be appropriate to answer if it may really bring fluidity in the process flow, if it really reflects transparency among other marvelous values and if who backs it is really reliable.

References

- Abolafia, Mitchell Y. 1998. «Markets as cultures: an etnographic approach.» In The Laws of the Markets, by Michel Callon, 69 – 85. Oxford: Blackwell.

- Airoldi, G., G. Brunetti, and V. Coda. 2005. Corso di Economia Aziendale. Milano: Mulino.

- Alchian, Armen A., and Harold Demsetz. 1972. «Production, information costs, and economic organization.» American Economic Review pp. 777 – 795.

- Bresnahan, T., and M. Trajtenberg. 1995. «General Purpose Technologies: Engines of Growth?» Journal of Econometrics (65): pp. 83 – 108.

- Callon, Michel. 1998. The Laws of The Markets. Oxford: Blackwell.

- Davidson, S., P. De Filippi, and J. Potts. 2016. «Disrupting Governance: The New Institutional Economics of Distributed Ledger Technology.» doi:http://dx.doi.org/10.2139/ssrn.2811995 .

- De Filippi, P., and A. Wright. 2018. Blockchain and the Law: The Rule of Code. London: Harvard University Press.

- De Filippi, Primavera, Morshed Mannan, and Wessel Reijers. 2020. «Blockchain as a confidence machine: The problem of trust & challenges of governance.» Technology in Society. doi:https://doi.org/10.1016/j.techsoc.2020.101284.

- Dhillon, Vikram, David Metcalf, and Max Hooper. 2017. Blockchain Enabled Applications. Orlando, Florida: Apress.

- Fligstein, N., and I. Mara-Drita. 1996. «How to make a market: Reflections in the attempt to create a single market in the European Union.» American Journal of Sociology 102 (1): pp. 1 – 33.

- Hayek, F. A. 1945. «The Use of Knowledge in Society.» The American Economic Review 35 (4): pp. 519 – 530.

- Jones, Kristopher. 2019. «Blockchain in or as governance? Evolutions in experimentation, social impacts, and prefigurative practice in the blockchain and DAO space.» Information Polity 24 (4): pp. 469 – 486. doi:DOI 10.3233/IP-19015.

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Resource accessed on April 10, 2021. https://bitcoin.org/bitcoin.pdf.

- Podolny, Joel M. 1993. «A Status-Based Model of Market Competition.» The American Journal of Sociology 98 (n. 4): 829-872.

- Polanyi, Karl. 1945. The Great Transformation.

- Preda, Alex. 2006. «Socio-technical agency in financial markets the case of the stockticker.» Social Studies of Science 36 (5): pp. 753 -782.

- Rikken, O., M. Janssen, and Z. Kwe. 2019. «Governance challenges of blockchain and decentralized autonomous organizations.» Information Polity 24 (4): pp. 397 – 417.

- Sinclair, Davidson, Primavera De Filippi, and Jason Potts. 2018. «Blockchains and the economics institutions of capitalism.» Journal of Institutional Economics 14 (4): pp. 639 – 685.

- Voshmgir, S. 2019. Token Economy: How Blockchains and Smart Contracts Revolutionize the Economy. Berlin: BlockchainHub Editions.

- Williamson, Oliver E. 1993. «Calculativeness, Trust, and Economic Organization.» Journal of Law and Economics 36: pp. 453 – 486.

- Williamson, Oliver E. 1973. «Markets and Hierarchies: Some Elementary Considerations.» The American Economic Review 63 (2): pp. 316 – 325.

- Williamson, Oliver E. 2008. «Outsourcing: Transaction Cost Economics and Supply Chain Management.» Journal of Supply Chain Management 44 (2): pp. 5 – 16.

- Williamson, Oliver E. 1981. «The Economics of Organization: The Transaction Cost Approach.» A cura di pp. 548 – 577. American Journal of Sociology 87 (3).

- Williamson, Oliver E. 1979. «Transaction-Cost Economics: The Governance Of Contractual Relations.» The Journal of Law and Economics 22 (2): pp. 233 – 261.